Search results

43 results found.

43 results found.

In Part Two, I explore two areas of focus in Credit Card differences. They are network versus co-branded credit cards in addition to secured versus unsecured credit cards.

I will answer Credit Card differences in Part Two of Different Types of CreditCards and Their Best Uses. The first question I will answer is, ‘Why get network cards’? Then, ‘Why get store co-branded cards’? And finally, ‘What is the difference’?

Referring back to Part One, it was explained that there are four types of major network credit cards, AMERICAN EXPRESS, DISCOVER, VISA, and MASTERCARD. Purchases can be charged just about anywhere with these cards. But there are no interest-free payment plans available.

In contrast, co-branded credit cards offer interest-free payment plans. This is what makes them an essential part of credit card differences. The banks that these cards cobrand with are rarely major banks. That is because their primary purpose is cobranding not checking, savings, etc.

Thus a prudent mix of both types of cards is the optimal way to benefiting from credit card differences, the best percentages of cash rewards available combined with interest-free, overtime purchase payments. The blog post A Two-Pronged Credit Card Rating System (Part 2 – June 2019) reviews the reason to get a straight flush scenario with the major network cards.

The above questions about network versus cobranded cards will be followed by an explanation of the difference between secured versus unsecured credit cards. On top of that, information about more cobranding banks that were mentioned in the last post will be discussed. Links will be provided in the SOURCES & RESOURCES area, as well.

Quoted from 5 Types of Credit Cards, “People who have a bad credit history or no credit history at all can take help of these secured cards. These secured cards are similar to that of general credit cards. However, in case of these cards, you must make a fully refundable deposit, either by cash or by sending a check. This deposited amount is considered as your credit line. As a result of this deposit, all the secured cards offer guaranteed approval.”

Quoted from the ‘General Credit Cards’ section from the same post, “General Credit Cards: A very common type of credit card is the general credit card. Such credit cards don’t require any kind of security deposit and can be used in most stores/shopping malls or to make any kind of purchases.” This definition would include what we call an unsecured, network credit card or co-branded card.

As stated earlier, there are really only two kinds of cashback credit cards, network and cobranded. In fact, the secured or unsecured featured is really just a qualification. But it is not its own category as the post 5 Different Types of Credit Cards states.

What Are Co-branded Credit Cards from The EXTraveler

5 Different Types of Credit Cards

Co-branded credit cards from Wallet Hub

Mixed cash rewards are the category of cards that most cash reward cards fit into. Therefore, this blog post will offer much details about this category. Unlike Green Go cards that have excellent ratings, these mixed benefit cards can have many pros and cons. Because of this, I refer to them as yellow light cards. Their mix of offerings can make it very difficult to decide whether to go or to stop from securing one.

In order to make the most of mixed cash reward credit cards, one should first compile a list of the pros and cons of the cards being considered. I recommend applying for only one card at a time. Let me explain how the mixed category works.

As described in previous posts in this series, Cash Reward credit cards can be divided into three types of benefit categories. This is similar to how a traffic signal directs vehicular activity. Both the GREENLIGHT and REDLIGHT signal are fairly straight forward in their comment. The former directs one to GO while the latter clear indicates STOP.

But the middle or mixed category does neither clearly. In fact, it leaves the decision up to the driver. That person must make a judgment call on their own. In spite of this, a judgment call does not have to be made blindly.

• GREEN LIGHT credit card cash reward cards detailed in the blog post Excellent Cash Reward Credit Cards (June 2019)

• YELLOW LIGHT cash reward cards and qualities are detailed in this blog post, Mixed Cash Reward Credit Card Benefits (June 2019)

• RED LIGHT means to seriously consider avoiding a particular cash reward card with overwhelming drawbacks.

So far, all the credit cards mentioned in this series have no annual fees. But cards that do have annual fees can pay substantially more rewards, like the Blue Cash Preferred Card from American Express®. For the privilege of the much higher cash reward levels, there is an annual fee of $95. Coincidently, there is also a signup bonus of $250. Right there, the annual fee is offset. For the most part, I prefer not to get cards with annual fees. Somehow, money needs to be made available to pay the fee each year.

This works well for people with savings. But it may not be practical for Former Middle-Class people who barely make ends meet on a monthly basis to allow for this. Saving up $95 for the annual fee tends to be a luxury reserved for the Middle Class. But, in spite of my limited funds, I made a judgment call and went for a card with an annual fee. My thinking was as follows.

Normally, I get 3% cashback for groceries. Figuring charges of around $400/month for groceries at 3% gives me a return of $12/month. That becomes $24/month at 6%. Over a year, I make an additional expense reduction of $120. That pays for the annual fee of $95. In addition, the promotional signup bonus is $250. This is clearly a win-win situation. I just have to make sure I have the annual fee put aside each year. Another point in its favor is that the total of necessary charges. It is $1000 in 3 months. That is the same as many other cards with fewer benefits.

Also, check the fit as described in the third post poker analogy. Does it fit into the % flush or straight flush? Does it have the most benefits for type category you want a card in? Refer back to Blog Post 3as a helpful example. Also refer to the example below.

If you are looking to form an ongoing credit card charging relationship with a home improvement superstore, controversy reign on which store and credit card are best. Lowe’s seems to outrank The Home Depot. Also see the review of the Barclaycard in the Sources & Resources Section at the end of this post.

[caption id="attachment_19475" align="alignleft" width="703"] At first glance, a great deal. But read the fine print.

At first glance, a great deal. But read the fine print.

Green Go cards are clearly transparent in what makes them excellent considerations for cash reward cards. Yellow mixed consideration cards are not as straight forward. Then, the pros and cons need to be weighed more carefully to decide if one in this category is a good choice. Consider the amount of a promotional bonus they pay. Know the % of return and any limitations regarding that. See which side of the scale they tip to, more pros or more cons.

Check the fine print. That means the not obvious, hidden qualities of the card. As a matter of fact, these can result in more negative than positive qualities. For example, the Barclaycard account sounds good at first glance. But it does have one major drawback. I know of no other card with this drawback. Surprisingly it does not pay cash rewards until $50 worth has been accumulated. So beware of such fine print. In addition, Some other cards charge no annual fee for the first year but do charge one after that.

The final post in this series will focus on the qualities and kinds of cards that are in the RED signal area. They should be avoided or pursued with the utmost caution. Because they are risky, sometimes that makes them plain unsuitable in my opinion. In addition, the risk is like making a right turn on red when you’re not sure there was a sign indicating that it is okay to do so. Or you make the turn without looking so see if a card is coming from your left. Beware Risky Cash Reward Cards

Here are the links to this five-part series about my Credit Card Rating System:

Introduction to A Credit Card Rating System

The Rating System Used for Cash Back Credit Cards (Series Part 2 – June 2019)

Excellent Cash Reward Cards (Part 3 – June 2019)

Mixed Cash Reward Credit Card Benefits (Part 4 – June 2019)

Risky Cash Reward Credit Cards (Part 5-June 2019)

Please note: I am not a certified financial planner or professional advisor. These blog posts about the use of credit cards are based on my own experience which I freely share. But I can take no legal or financial responsibility for the results you may have in attempting to follow my system. But I do wish you the best and welcome your comments and questions at the VERY end of this post. You will have reached the end because you can not scroll down any further. As well, you will have reached the comment form.

Compare Cards: Best Cards for Cash Back

Nerd Wallet | Credit Cards Market Place

How Cash Back Credit Cards Work

Credit Cards for Home Improvement

Barclaycard CashForward World Mastercard

This post, excellent cash reward cards is the third in this series. By now readers most likely understand that in order to choose excellent cash reward cards including the excellent benefits they offer, it is key to have a reliable cash reward credit card rating system. Then one can best evaluate the quality of any card being considered.

As a rule, cash reward credit cards offer all kinds of cash benefits as compensation for making purchases with them. In order to make the most of cash reward credit card choices, you need to know a card’s pros and cons.

As a matter of fact, excellent cash reward cards tend not to have much of anything in the way of drawbacks. In other words, you want to pick a card that bats as close to 1000 as possible. That is the purpose of an excellent cash rewards card.

With this in mind, once you know what to look for and what to avoid, then you’ll have the tools necessary to plan for the best card with the most benefits. In other words, an excellent rated card. Let’s look at this more closely.

Greenlight cash reward credit cards offer these types of benefits:

1. good to excellent percentages on cash rewards (3-5%)

2. $150-$200 promotional bonus for opening an account and even more on cards with annual fees

3. cash rewards are available in any amount at any time

4. rewards redemption is possible by a variety of methods

5. choose from several categories for top rewards rate

6. payment date and statement closing dates can be changes

The benefits include:

a. $200 promotional signup bonus

b. 3% reward in a specific categories

c. user can choose which category gets 3% from several options

d. cash rewards accumulated are available in any amount at any time

e. no annual fee

The benefits include:

a. $150 promotional signup bonus

b. 1.5% everywhere, on everything

c. redeem any amount of rewards at any time

d. no annual fee ever

There’s more to come. Here are the links to all five posts in this series about my Credit Card Rating System:

Introduction to A Credit Card Rating System

The Rating System Used for Cash Back Credit Cards (Series Part 2 – June 2019)

Excellent Cash Reward Cards (Part 3 – June 2019)

Mixed Cash Reward Credit Card Benefits (Part 4 – June 2019)

Risky Cash Reward Credit Cards (Part 5-June 2019)

Please note: I am not a certified financial planner or professional advisor. These blog posts about the use of credit cards are based on my own experience which I freely share. But I can take no legal or financial responsibility for the results you may have in attempting to follow my system. But I do wish you the best and welcome your comments and questions at the VERY end of this post. You will have reached the end because you can not scroll down any further. As well, you will have reached the comment form.

Nerd Wallet | Credit Cards Market Place

Best Cash Back Credit Cards from WalletHacks.com

I’ve developed a credit card rating system that is very helpful in choosing Cash Reward Credit Cards. Specifically, the system analyses what particular cash rewards credit cards can and can’t do to help lower my monthly charged expenses at any given time.

To start, the first part of the system is analogous to how a traffic signal operates. In other words, Cash Reward Credit Cards offer percentages of cash benefits to cardholders for charging purchases on their cards. Then, there are a variety of different qualities to benefit from.

To make the most of cash reward credit cards, become familiar with the benefits of all the cash reward credit card accounts being considered. As a refresher to the first post in this series, cash reward credit cards use can be divided into three benefits categories. For example, this is similar to a three-colored traffic signal. Thus, I have named the cash reward credit cards as reflections of the actions to take in response to traffic signal lights:

GREEN LIGHT indicates a clear go-ahead signal

YELLOW LIGHT suggests proceeding with some degree of caution

RED LIGHT urges avoiding or proceeding at one’s own risk

Study and choose carefully. As mentioned, this is because cash reward credit cards do not all have the same qualities or rates of return. In fact, they can be very different. As a result of studying each card’s personality, one will become familiar with the specific qualities. That way, a person will have an idea of how to plan for the most beneficial outcome. This means studying how best to use each card on its own. It includes observing the power of using them in combination with others.

In fact, cash reward credit cards work best as a team. Let me explain how this works. Different cards offer a different % of cashback for different categories of purchases. Thus, the ideal situation is to gather a group of the highest rate of cash return for each of the card categories that one uses most. For example, if one charges mostly for groceries and gas each month, the goal would be to acquire cards that pay the highest rate in these categories. In fact, these days that can be between 3% to 5%, and even 6%.

Ironically, credit card teamwork actually reminds me of a winning hand in the card game of poker. In comparing the two, one would want to come up with cards of the same suit. But each with a different card in numerical order. This is known as a straight flush. See the example above. In actuality, the only difference is that in the game of poker there are only 5 playing cards. But in my credit card system, there are ideally 6 credit cards. Therefore, a winning hand would be 6 cards with these percentages in the categories listed:

6% for US supermarkets

5% for all purchases on a store card

4% for dining out

3% for gas

2% for health care

1.5% for all purchases

Here’s a tip from James Wang of WalletHacks.com. Be certain to label credit cards with a magic marker to remind you what card to use for what category of purchase and % of the return. By doing this, you won’t forget and use the wrong card. Remember, you want to get the highest percentage of cash return out of each purchase. For that reason, this clever trick is invaluable.

Note that the next three blog posts in this series will specifically explore two things. First, each of the qualities of cash reward credit cards will be explored. Then specific cards will be analyzed. An easy way to remember the categories is Green for GO, Yellow for CAUTION, and Red for AVOID or proceed at your own risk!

Here are the links to all five posts in this series:

Introduction to A Credit Card Rating System (Series Part 1 – June 2019)

The Rating System Used for Cash Back Credit Cards (Series Part 2 – June 2019)

Excellent Cash Reward Cards (Part 3 – June 2019)

Mixed Cash Reward Credit Card Benefits (Part 4 – June 2019)

Risky Cash Reward Credit Cards (Part 5-June 2019)

Please note: I am not a certified financial planner or professional advisor. These blog posts about the use of credit cards are based on my own experience which I freely share. But I can take no legal or financial responsibility for the results you may have in attempting to follow my system. But I do wish you the best and welcome your comments and questions at the VERY end of this post. You will have reached the end because you can not scroll down any further. As well, you will have reached the comment form.

Credit Card Categories, Sign Up Incentives and Cash Rewards

Nerd Wallet | Credit Cards Market Place

The Former Middle Class Ebook Series

U.S. News’ 10 Best Cash Back Credit Cards

The responsible use of cash reward credit cards has been very helpful in reducing my monthly expenses. In order to help me decide what new credit card I should apply for at any given time, I have developed a credit card rating system. It guides me in determining which credit card will best meet my needs at the time I apply for it. This blog post series will explain my system in detail to help others decide what cards and card qualities to consider as well.

The categories of credit cards are shown in the illustration below. Note that each serves a different purpose. Cash reward credit cards provide a crucial feature that some of us value most, cash back for a reduction in expenses. To apply the system where it has great value, I will use the cash back or cash rewards cards category as the primary focus of this blog post series, A CREDIT CARD RATING SYSTEM.

With cash back credit cards, one can get reductions in monthly credit card charges. This is crucial for the survival of someone who is a Former Middle-Class Person as well as a senior citizen. In fact, the benefits offered to make life easier with these cards increases almost daily. This is because credit card issuers are becoming increasingly competitive with generous offers to lure new customers to switch credit cards.

It can be preferable to add a new credit card rather than switch by elimination. On the other hand, there are many details to keep in mind when adding rather than switching. In spite of that, one major benefit of having a bounty of (cash reward) credit cards is a substantial amount of total available credit. This means that if a credit cardholder uses a very small % of his/her total available credit each month, a major factor of one’s credit score remains ‘EXCELLENT’. When it comes to credit scores, most systems use a total of six factors and using a small % of available credit is one of them. But adding new cards definitely has its pluses and minuses. In spite of the challenges, I have found adding cards to be a plus. More about this in the other posts in this series.Here is an article about this from Credit Karma.

The additional posts in this series will focus on how my credit card rating system relates to how I choose cash rewards credit cards. I can and do use it for deciding on all my accounts. The beauty of this system is that it can be used across the board with any cash reward card. In fact, it can be used for deciding on any type of credit card as well.

Here are the links to this five part series about my Credit Card Rating System: Introduction to A Credit Card Rating System

The Rating System Used for Cash Back Credit Cards (Series Part 2 – June 2019)

Excellent Cash Reward Cards (Part 3 – June 2019)

Mixed Cash Reward Credit Card Benefits (Part 4 – June 2019)

Risky Cash Reward Credit Cards (Part 5-June 2019)

Please note: I am not a certified financial planner or professional advisor. These blog posts about the use of credit cards are based on my own experience which I freely share. But I can take no legal or financial responsibility for the results you may have in attempting to follow my system. But I do wish you the best and welcome your comments and questions at the VERY end of this post. You will have reached the end because you can not scroll down any further. As well, you will have reached the comment form.

To learn more about credit card cash rewards, go to these blog posts:

Credit Card Categories, Sign Up Incentives and Cash Rewards

How To Compound Cash Rewards

Nerd Wallet | Credit Cards Market Place

The Former Middle Class Ebook Series

The learn more about all kinds of credit cards, go to following link about CompareCards.com (A.) and its sublinks (B. through I.)

A. CompareCards® by Lending Tree

B. Best Credit Card Offers July 2019

C. Low Interest Cards

D. Balance Transfer Cards

E. Cash Back Cards

F. Reward Cards

G. Airline Cards

H. Business Cards

I. No Annual Fee Cards

There are numerous credit card categories and signup incentives available. For example, some credit cards offer hefty signup bonuses. Others have top cash rewards. Then there are travel points. Finally, there is balance pay down cards. You just have to know what you need, go over the details, see what you qualify for, and apply for the best card in that category. Because there is so much to cover, this blog post will focus only on one time sign up cash incentives and ongoing cash rewards.

There are basically two ways that credit card companies entice new customers seeking cash rewards as their priority. First, there is a single signup cash back bonus. This is accomplished by offering a set amount of money to be charged on a new credit card within a given amount of time. In addition or instead, there can be ongoing cash rewards.

This particular card is a very good deal all around. It offers a number of excellent credit card signup incentives. In fact, it is ideal for someone seeking a credit card with cash rewards:

• $150 cash reward bonus

• cash back on every purchase, every time

• no annual fee†

• your choice of a 3% cash back category, 2% and 1% categories

Let’s compare the Bank of America VISA Cash Rewards Card with some of my other favorites. In fact, I have several other favorites. Determining which are the best cards or even single card depends on a person’s credit card charging needs or spending profile, as I like to call it. For example, I always aim to get the maximum cash back on every purchase I make. Therefore, when I signup for a card, I like to make sure it fits into my spending profile. For example, these are my major credit card charging categories:

• GROCERIES

• DINING (EATING OUT)

• UTILITIES

• GAS

• HEALTHCARE

• HOME AND PERSONAL PURCHASES

Here is how my system works. For example, the American Express Blue Everyday card offers 3% cash back so that is my card of choice for groceries. It has a similar profile to the Bank of America® card with a few differences.

• $150 or $200 cash reward bonus

• cash back on every purchase, every time

• no annual fee†

• 3% cash back on groceries

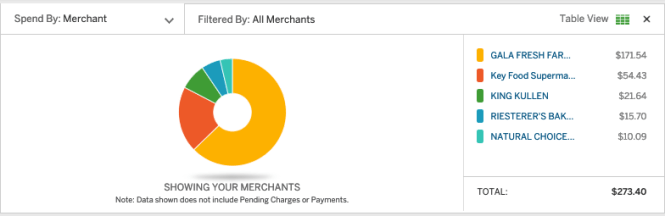

Numerous credit card accounts provide charts like the this one to provide of breakdown of categories of expenses or vendors within a particular category.

This card offers 4% for dining out. It even includes McDonald’s, Burger King, Dunkin Donuts, etc. .

.

The chart below compares values of dining out cards. The Savor Card is close to the highest and charges less than others with higher or similar % bonuses.

This is how I break in a new credit card to receive their one time sign up bonus. If I use it to charge my monthly utility bills such as cable, cell phone, and contents insurance, I charge about $275 a month on it. That easily covers a requirement of $500. in charges in two months. A requirement of $1000 in charges in three months can also be covered with a few extra charges are added in. I have fulfilled the requirements of a number of very useful cards with this method. In addition, I also get monthly cash rewards this way because I use the new card for charges and pay it the following month from my checking account. This technique is a real winner if I can remember which month I am supposed to do what task.

Because Bank of America® Cash Rewards Cards now offers the option of choosing 3% on their new ‘Choose Your Category’ plan, we use it to pay for gas. That is the best cash back rate I have found to date for gas.

The CareCredit® Rewards Master Card pays 2% on health related and other charges that the above and below cards do not cover for more than 1% or 1.5%

*Subject to credit approval.” Quoted from CareCredit® Card’s application material.

TJ Maxx which includes Home Goods, Marshalls and Sierra have special promos that can triple their usual ratio of points for each dollar spent. On the other hand, Home Depot has a $25 signup bonus which is deducted from the first purchase only. There is no cash reward bonus for their card.

As a result of careful planning, almost every charged purchase can earn a cash reward of between 1.5 % TO 5%. One exception is HOME DEPOT. They don’t offer cash rewards. So, from maximum to minimum, this is what a winning hand of credit card cash rewards might look like.

HOME, OFFICE AND PERSONAL: 5% Staples, Target*

DINING AND EAT OUT: includes McDonald’s, Burger King, Dunkin Donuts, etc. 4% Capital One® SAVOR Card

GROCERIES: 3% American Express® Blue Everyday Cash Rewards

GAS: Choose 3% on the new BoA ‘choose your category’ plan

HEALTH-RELATED, PET AND SOME BEAUTY: 2% CareCredit® Rewards MC 2%

EVERYTHING ELSE: 1.5% Capital One® Quicksilver card

*Special offers triple points at certain times of the year

Jim Wang of Wallet Hacks has the best trick I’ve heard of to remember which card offers what. Write it directly on the card. For example, on the Capital One® Savor Card write, ‘DINING 4%’. Just one word to describe the category and the % reward. It works very well when you have three, four, or even five cards in your wallet.

Wallet Hacks

Target

Staples

TJx Credit Cards

Capital One® Savor Card

Capital One® Quicksilver Card

American Express® Blue Cash Everyday Card

Bank of America® Cash Reward Cards

CareCredit® Rewards Card

Credit card cash rewards can offer added benefits to credit card owners. But sometimes it can be confusing to claim them. In addition, not all cash rewards are the same.

There are several types of credit card cash rewards as well as different ways they can be distributed. It is important to know when and how they can be made available to make the most of these rewards.

There are between three and four types of cash rewards. The most direct is the statement credit applied directly to your credit card statement, illustrated above. But which statement is the question. Is it your current statement or your next statement? I often find that a call into the credit card company is needed to clarify this question.

The other types of cash rewards are illustrated here. They are gift cards, merchandise and friend referral rewards.

This is where things can get confusing. Distribution has several options:

• anytime by request online or by phone

• with a minimum of $25 in rewards by the same methods

• in increments of $25 in rewards by the same methods

Option One is the simplest and most direct. Capital One and now Bank of America credit cards both offer this service. See the illustration above,

Option Two is where things can get complicated and there are drawbacks. This is because you can’t withdraw cash rewards at any time. There has to be an accumulation of at least $25 to do so. American Express distributes cash rewards this way. Read the fine print inside the red outline.

Then there is Option Three, the least desirable way to cash in cash rewards. They can only be made in increments of $25. As illustrated below, cash rewards can be distributed only in increments of $25.

Reading the fine print is important to understand what types of credit card cash reward exist and how they can be distributed. You can also learn more about credit cards on this blog by going to the search bar and typing in credit cards.

Capital One Cash Back VISA Credit Cards

Bank of America Cash Back VISA Credit Cards

Wells Fargo Credit Cards

American Express Credit Cards

My goal, as a retiree on a very fixed income as well as a member of The Former Middle Class is to make ends meet on a monthly basis. I find that Using Credit Cards for Survival and Profit is very helpful to accomplish that. But in order to do this, a credit card accounts maintenance system is necessary. Because I have used my system religiously, I have graduated to Mastering The System of Extreme Credit Card Benefits. The purpose of this post is to describe my system in detail so that you might be able to take these steps to make ends meet, too.

Because my credit card accounts maintenance system is so effective, I can manage a substantial number of credit cards responsibly and profitably. Even as the number of credit cards has increased, it has not interfered with my accounts staying in order. In addition, my credit scores continue to hover between 780 and 800, my credit report profiles are in good standing and I have very good to excellent credit.

I’ve developed a Credit Card Accounts Maintenance System that consists of a set of tools combining old fashioned manual bookkeeping techniques with up-to-date digital tools:

1. credit card information chart

2. manual ledger paper spreadsheet

3. digital bookkeeping program with checking ability

4. manual checking account with a colorful checkbook cover, checks and paper register

5. email access to and from all my accounts

6. online account access to each credit card listed in my bookmarks

7. online bill paying capability

8. telephone contact with each credit card company

I created a table in Microsoft Word®. It consists of the data for all my credit cards. That includes every bit of pertinent information about each card. There are even icon size images of all my credit card for visual recognition and order. See the categories shown below this illustration.

Perhaps because I grew up in the paper world before the computer, I still find it easier to use manual ledger paper for my credit card accounts maintenance system. But if I become more comfortable with Excel, I might shift my spreadsheet to Microsoft Excel®. Digital or manual, it is possible and prudent for me to keep a tally of every dollar I have charged on each card. Actually, all my tools create a checks and balances system to make sure my accounts are accurate. It doesn’t matter if they are manual or digital. Use what works for you.

Because I have a Macintosh Computer, I got the only bookkeeping program that was specific to Apple many years ago. It was originally called, MYOB an acronym for ‘Mind Your Own Business’. The name was updated to Accountedge because it now has many accounting features in addition to its original bookkeeping features. Accountedge.

I still pay a few bills manually using checks. Doing this makes it possible for me to keep track of certain personal loans as I pay off them off. This way I have a check copy on my monthly statement for record keeping and documentation. The purpose of my Checkbook Register is to keep a record of every financial transaction I make. I even devised a system of color coded symbols that shows when:

a. a purchase was made

b. it is recorded online by my bank

c. I entered it into my online bookkeeping system

The Credit card companies contact me by email. They remind me when bills are due and let me know if there is some other issue concerning my account.

I bookmark every credit card URL so that I can easily check each credit card account daily. This is another way for me to make sure that the numbers online coincide with my manual spreadsheet numbers.

Each credit card websites is listed on my Internet bookmarks to be accessed easily. Most of my bills are paid on line. Some are even on autopay. When I get a new card, I have my closing and bill paying dates adjusted so that my payment is due shortly after my monthly fixed income arrives. This way I can get all of my bills paid on time and not have to think about whether or not I paid them all month long.

Having telephone contact is very important. One can use any phone, a landline or cell phone. I make telephone contact with each credit card company when I have questions about my balance, closing or due dates.

Since most of these companies are open 24/7, I enjoy calling very early in the morning. It is usually the quietest time at their end. I’ve enjoyed hours of what become personal interest conversations with their staff who are located around the globe. It is fascinating and one of my favorite tools. In fact one call was such a delight for both of us that the customer service person from Capital One actually sent me flowers!

As I mentioned in the previous post, if a person needs or desires to have many credit cards, it is prudent to keep a very close watch on them in order to maintain a good relationship with each company as well as the credit reporting bureaus. This involves accurate reporting to keep my credit score high, to pay all my bills on time and stay within my budget. Because having many cards is based on need, I am very careful about using them responsibly. It is essential for me to be able to I continue to make use of what has helped me to make ends meet since we became part of The Former Middle Class. Extreme credit card benefits have been a tremendous help to me in making ends meet.

Wilson Jones Ledger Sheets Pad

Accountedge Accounting and Bookkeeping Program

Checks and register from checkworks, inc.

Word Tables

Excel Spreadsheets

1-800-Flowers

Telephone from lifehack.org

Capital One

Credit Reports

Before extreme credit card benefits can become a consideration for someone in The Former Middle Class, two things need to be explained. The first is that one must be thoroughly versed in The Principles of Good Credit Card Hygiene. Even if someone has a history of medicore credit, the credit score must become very good to excellent. ‘One Must Learn to Walk Before One Can Run’.

In contrast, there are people who can achieve even more extraordinary benefits than those of us who are part of The Former Middle Class can. That is because they have the funds to spend from the start. For example, one of the super benefits credit cards requires an expense of thousands of dollars to receive a heftier signup bonus. But in my case, I had started using credit cards with monthly bonuses to add a small amounts of cash to my retired, minimal fixed income.

During the time I was getting this kind of ordinary cash bonus of between 1% and 3%, I developed the need to acquire a travel point credit card offering both a cash rewards bonus and travel miles. That was when I became aware of the extreme benefits I could receive separate and apart from using credit cards the way I had been. The fact that both my husband and I had credit scores hovering around 800 helped tremendously to move into this new level credit card benefits, the sign up promotion.

As explained in the last blog post, a very good to excellent credit score is one of the most important aspects of qualifying for extreme credit card benefits. But let’s go back a step to when credit cards had cash rewards that paid out in increments of a minimum of $25. It was not difficult to earn about $40 over a two month period. But that is not extreme credit card benefits and I needed extreme benefits.

Extreme credit card benefits involve more than just getting monthly cash rewards or travel points. They require additional incentives from the credit card company to get someone to apply for a particular credit card. So that is exactly what the credit card companies started doing. They began to offer either large sign up cash or travel points promotions or both when a certain amount of money was charged by the customer in a given amount of time. The cash usually ranges between $100 and $200. Payment occurs after $500 or $1000 in charges. The period of time to make the charges is usually 3 months.

People who are solidly middle class can make a lot more cash back. But if one compares the percent of return rather than the cash itself, someone in The Former Middle Class can match and even outrank the returns that the Middle Class and above can. In one situation, I got a 40% sign up promotion cash bonus! I only had to spend $500 over a three month period. So $200 cash back from $500 spent is a 40% return. This is definitely Mastering The System of Extreme Credit Card Benefits.

We know that the first and most important thing is to achieve and maintain very good to excellent credit. The next thing is to apply for such a card after you have paid your balance in full and have zero debt. Lastly, it is important not to apply for too many credit cards in a short amount of time. Straight forward? So it would seem. But it can get complicated and time consuming requiring a actual bookkeeping system to stay on top of things. This will be discussed in a future post. This is the system of tools that I use to keep track of my extreme credit cards benefits card accounts.

It can become very enticing to continue to apply for and collect extreme credit card benefits cards. They offer a one time promotion that is a lot more than regular cash rewards or travel points. But one must proceed with caution by keeping diligent track of all of one’s accounts as the number of the hot credit cards in one’s possession increases. If a person accumulates a large number of these cards, it can become a job just keeping track of everything. Obtaining these cards can be a way to earn some extra non taxable income for The Former Middle Class person. But at the same time, unless it is a real necessity, it is easier to have a few top notch cards that offer cash back and are “tied to a travel program like an airline or a hotel”. According to Jim Wang of WalletHacks, they offer the best bonuses.

The Former Middle Class

Wallet Hacks, Best Credit Card Promotions

Using Credit Cards for Survival and Profit

The Principles of Good Credit Card Hygiene

Mastering The System of Extreme Credit Card Benefits

The Credit Card Maven

Savvy Saving Survivalism

Good Credit Card Hygiene is based upon several principles. They are the focus of and shall be reviewed in this blog post. Before any discussion can be held about extreme credit card benefits, one must have a firm grasp of the basic principles especially the components of your credit score.

To start with, it is very important to gain and maintain between a very good to excellent credit rating. Even if your credit is poor to start with, there are many resources, both nonprofit and professional that can help you to raise your credit or FICO® score. See the pie chart below for the breakdown of components.

Payment history has top billing in the equation. It is crucial to always pay your monthly bills in full and on time. This is the first of the five components of your credit score and counts for 35% of the credit score algorhythm. You could say that it is the key player in good credit card hygiene.

The next component that counts for 30% of your credit score is your level of debt. What this means is that the amount you owe or your monthly debt should not comprise more than 30% of the entire amount of credit that has been made available to you. If your total credit allocation is $100,000 then you should charge less than $30,000 each month. Actually, the most recent numbers I have heard, are that the credit reporting agencies are looking for a percentage of between 6-9%. This means that one’s monthly debt (credit card charges, loans, mortgage payments, etc.) should not exceed between $6,000 to $9,000.

The first two factors make up 65% of your score so clearly they are the most important ones in obtaining and maintaining good credit card hygiene. Next is the age of your credit which makes up 15% of your score. Start applying for a credit card as early on as you can so that you will have a long credit history. In order to increase your chances of getting one, apply for a card for which you have been pre-approved. That way your credit score will not go down because of your application. Picking out a card that has not be pre approved will result in the reduction of your credit score whether you get the card or not. But it may not be a serious problem. You can still have good credit card hygiene and a decent FICO score.

Now you have 80% of your credit score accounted for. These are the three most important factors. But don’t ignore the others. It is good credit card hygiene and good for your score to have a mix of types of debt, credit card, loans, and/or mortgage. Here again, since this makes up only 10% of your score, it is not crucial. Likewise, credit inquiries also make up 10% of your score. So they are not crucial either.

There are numerous types of credit score systems, each with its own algorhythm. Two of the most popular systems are shown above FICO and Vantage. FICO® was created by the Fair Isaac Corporation. VantageScore is comprised of the input from these three reporting agencies, TransUnion, Equifax and Experian. They do not have the same exact rating scales but the difference is not far off. So let’s continue with the characteristics of good credit card hygiene.

Do not apply for too many cards in a short period of time. You will know that you are applying for too many in too short a time if you start getting rejections and that is the reason the credit card company gives for it.

Be mindful to not do anything that will result in negative comments on your credit report. If you do, these will reflect poorly on your credit score. This is not considered good credit card hygiene.

Check your credit card activity often and your credit scores regularly. Now that most, if not all credit card companies have this as a free feature, it is very easy to do. If you find any errors on your credit card, contact the company immediately. If you suspect fraud, contact the police as well as the credit reporting agencies. This can be very serious. Do this in a timely matter.

It is recommended not to close credit card accounts especially old ones. But if you must, wait until you have zero debt to do so. You don’t want to negatively affect you debt to available credit ratio.

That’s about it for a review of what good credit card hygiene is. Once you have established a level of comfort and confidence with it, you can move on to the exciting part, Extreme Credit Card Benefits. That is the topic of the next blog post. I promise you will be WOWed by it.

Using Credit Cards for Survival and Profit

15 Credit Card Do’s and Don’ts